The $95,093.35 Fake Check That Became A Big Headache

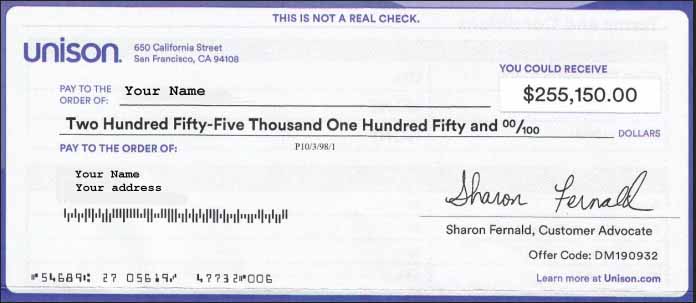

Pictured above (via some website I found) is something that looks like a check for $255,150, but it’s not actually a check. The big clue? The words “This is not a real check” at the top of the non-check check. (The “Your Name” and “Your address” placeholders are also pretty solid clues. If you were to bring it to your bank, they’d probably look at your strangely and maybe laugh at you. But they almost certainly wouldn’t put $255,150 in your bank account.

Almost certainly.

Just ask Patrick Combs.

It’s not uncommon for marketers to mail real-ish looking fake checks to would-be customers. The idea is simple: most such “junk mail” barely gets a glance before it goes into the recycle bin or the trash, and that’s a bad outcome if you’re the marketer. But if you send someone something that looks like a check, there’s a pretty good chance the consumer will give it a second look before similarly dooming it for the bin. And sometimes, that second look is all the seller needs to make their sale.

No one — not the marketer, not the consumer, and definitely not the bank — expects someone to take that fake check and deposit it into their bank account. But in May 1995, Combs, an author with a national bestseller to his credit, decided to do just that. He received a promotional fake check in the amount of $95,093.35 but didn’t just throw it out. As he wrote in the Financial Times, “as a joke, I deposited the fake cheque into my bank’s ATM. I felt like a million bucks doing so. I’d never had so much fun at my bank. Come to think of it, I’d never had any fun at my bank until the moment I endorsed the back of this ‘cheque. with a smiley face and slipped the Monopoly-like money into the mouth of the hungry ATM. For the first time ever, I walked away from my bank laughing.”

Combs assumed the bank would just reject the clearly-fake check and he all but forgot about the joke deposit. But about a week later, he went back to the ATM to withdraw some cash and his bank balance was much, much higher than expected. The bank had honored the check.

He decided to play it safe, knowing that the the check wasn’t real and that he wasn’t entitled to the money. He went to a law library to see what the rules around bank errors were, and what he found suggested that the money was his. After another week or so, he asked the bank’s branch manager, who also told him that after ten days, a check can’t bounce, and as that period had passed, he was in the clear. Still skeptical — and assuming that the junk mailer would ultimately want their money back — he decided to protect himself while also withdrawing the funds. He asked the bank to cut him a cashier’s check matching the amount of the fake check, and then he placed that cashier’s check in a safe deposit box within the same bank.

About a month later, the bank noticed the error — and they weren’t nice about it. As the New York Times reported, the bank froze Combs’s account and when he went to use the ATM, the machine ate his card. And that was only the beginning. The Times continues: “a bank security officer called Mr. Combs and demanded the money back. But when Mr. Combs said he was on vacation and could not get to the safe deposit box, the security officer demanded permission to drill the box open.” Combs initially was more than willing to return the money, but given the bank’s aggressive approach upset him and shattered his trust in the institution. He refused to comply until they issued him a letter detailing the situation, as he outlined in the above-linked Financial Times piece:

My response to the bank’s security officer was simple: “Give me a letter on official bank stationery stating that you are who you say you are, that you indeed work for the bank, and also put in that letter the reason why the bank is requesting the money back, as I’m a little confused on that. When I get that letter we’ll go from there.” And his response, to paraphrase and keep this article profanity-free, was: “Never!”

The back and forth went on for months. The bank threatened to get authorities involved, which is strange because it wasn’t clear that the law was on their side. The press hooked onto his story and the general public was involved shortly thereafter, with the majority (per Combs) saying he should keep fighting the bank and/or take the money.

Ultimately, the bank wrote him that letter and he capitulated. As the New York Times briefly noted in October — five months after Combs deposited the fake check — he returned the real cashier’s check to the bank.

Combs came out ahead, though — he turned his story into a one-man comedy show and ultimately, a book. Whether it made him more than $95k? That’s gone unreported, but at least he got to keep that money.

Bonus fact: In general, banks pay better attention to deposits than they did in the story above. And that level of attention likely thwarted the first notable bank robbery in American history. In the fall of 1798, a carpenter named Isaac Davis conspired with a bank porter named Thomas Cunningham to steal $162,821 (about $3 million in today’s dollars) from the Bank of Pennsylvania at Carpenters’ Hall in Philadelphia. And they likely would have gotten away with it — the authorities arrested the blacksmith who helped forge the vault, Patrick Lyon, almost immediately (even though Lyon turned out to have no involvement and an air-tight alibi). But Davis did something dumb. As the Carpenters’ Hall website recounts, “Then in a move that will live in the annals of stupidity, Davis began depositing the missing money in the very bank he had robbed and other Philadelphia banks, casting suspicion on himself.” Davis didn’t go to jail though; after some (likely corrupt) backroom dealings, he was able to secure a pardon in exchange for returning the money.

From the Archives: Why You Shouldn’t Take Advice from a Board Game: The bank error that was definitely not in their favor.